Medicare Benefit ŌĆō the economic choice to conventional Medicare ŌĆō is drawing down federal well being care budget, costing taxpayers an additional 22% in step with enrollee to the music of US$83 billion a yr.

Medicare Benefit, sometimes called Section C, used to be meant to avoid wasting the govt cash. The contest amongst personal insurance coverage firms, and with conventional Medicare, to regulate affected person care used to be intended to offer insurance coverage firms an incentive to seek out efficiencies. As a substitute, this systemŌĆÖs cost regulations overpay insurance coverage firms at the taxpayerŌĆÖs dime.

WeŌĆÖre well being care coverage professionals who learn about Medicare, together with how the construction of the Medicare cost machine is, when it comes to Medicare Benefit, running towards taxpayers.

Medicare beneficiaries select an insurance coverage plan after they flip 65. More youthful folks too can turn into eligible for Medicare because of persistent stipulations or disabilities. Beneficiaries have a number of choices, together with the standard Medicare program administered via the U.S. authorities, Medigap dietary supplements to that program administered via personal firms, and all-in-one Medicare Benefit plans administered via personal firms.

Industrial Medicare Benefit plans are increasingly more common ŌĆō over part of Medicare beneficiaries are enrolled in them, and this proportion continues to develop. Persons are attracted to those plans for his or her further advantages and out-of-pocket spending limits. However because of a loophole in maximum states, enrolling in or switching to Medicare Benefit is successfully a one-way boulevard. The Senate Finance Committee has additionally discovered that some plans have used misleading, competitive and probably destructive gross sales and advertising and marketing techniques to extend enrollment.

Baked into the plan

Researchers have discovered that the overpayment to Medicare Benefit firms, which has grown through the years, used to be, deliberately or now not, baked into the Medicare Benefit cost machine. Medicare Benefit plans are paid extra for enrolling individuals who appear sicker, as a result of those folks most often use extra care and so can be costlier to hide in conventional Medicare.

Alternatively, variations in how folksŌĆÖs diseases are recorded via Medicare Benefit plans reasons enrollees to look sicker and more expensive on paper than theyŌĆÖre in actual lifestyles. This factor, along different changes to funds, ends up in overpayment with taxpayer greenbacks to insurance coverage firms.

A few of this additional cash is spent to lower price sharing, decrease prescription drug premiums and building up supplemental advantages like imaginative and prescient and dental care. Regardless that Medicare Benefit enrollees might like those advantages, investment them this fashion is pricey. For each and every further greenback that taxpayers pay to Medicare Benefit firms, most effective more or less 50 to 60 cents is going to beneficiaries within the type of decrease premiums or further advantages.

As Medicare Benefit turns into increasingly more dear, the Medicare program continues to stand investment demanding situations.

In our view, to ensure that Medicare to live to tell the tale long run, Medicare Benefit reform is wanted. The best way the govt will pay the personal insurers who administer Medicare Benefit plans, which might appear to be a black field, is vital to why the govt overpays Medicare Benefit plans relative to conventional Medicare.

Paying Medicare Benefit

Non-public plans had been part of the Medicare machine since 1966 and feature been paid thru a number of other programs. They garnered just a very small proportion of enrollment till 2006.

The present Medicare Benefit cost machine, applied in 2006 and closely reformed via the Inexpensive Care Act in 2010, had two coverage objectives. It used to be designed to inspire personal plans to provide the similar or higher protection than conventional Medicare at equivalent or lesser charge. And, to ensure beneficiaries would have a couple of Medicare Benefit plans to choose between, the machine used to be additionally designed to be successful sufficient for insurers to trap them to provide a couple of plans all over the rustic.

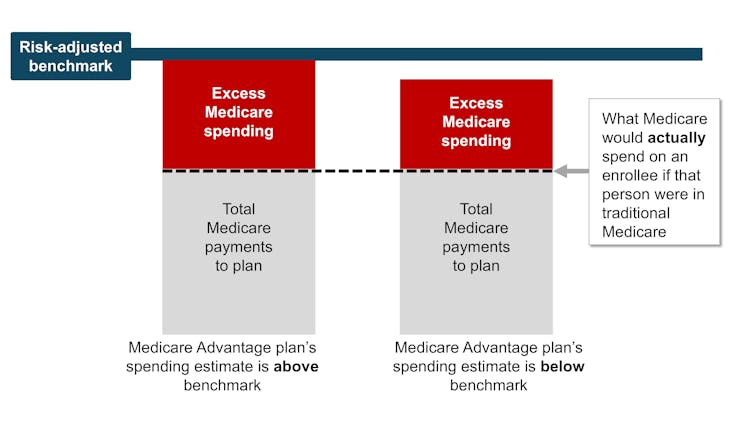

To perform this, Medicare established benchmark estimates for every county. This benchmark calculation starts with an estimate of what the government-administered conventional Medicare plan would spend at the moderate county resident. This worth is adjusted in line with a number of components, together with enrollee location and plan high quality scores, to offer every plan its personal benchmark.

Medicare Benefit plans then publish bids, or estimates, of what they be expecting their plans to spend at the moderate county enrollee. If a planŌĆÖs spending estimate is above the benchmark, enrollees pay the variation as a Section C top rate.

Maximum plansŌĆÖ spending estimates are under the benchmark, alternatively, which means they mission that the plans will supply protection this is an identical to conventional Medicare at a lower price than the benchmark. Those plans donŌĆÖt rate sufferers a Section C top rate. As a substitute, they obtain a portion of the variation between their spending estimate and the benchmark as a rebate that theyŌĆÖre meant to go directly to their enrollees as extras, like discounts in cost-sharing, decrease prescription drug premiums and supplemental advantages.

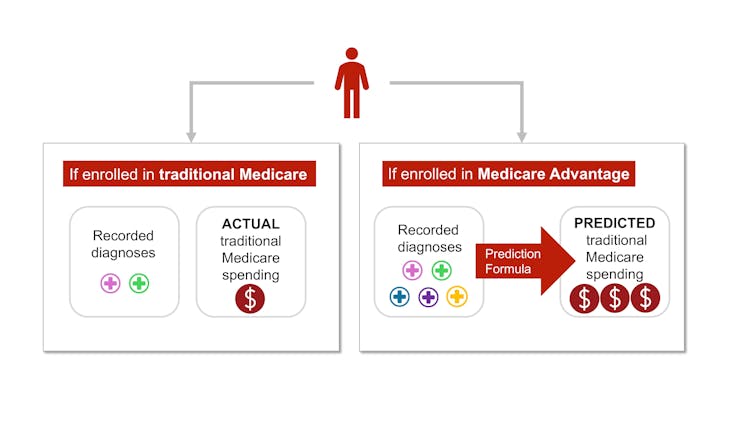

In the end, in a procedure referred to as menace adjustment, Medicare funds to Medicare Benefit well being plans are adjusted in line with the well being in their enrollees. The plans are paid extra for enrollees who appear sicker.

The federal government will pay Medicare Benefit plans in line with MedicareŌĆÖs charge estimates for a given county. The benchmark is an estimate from the Facilities for Medicare & Medicaid Products and services of what it might charge to hide a mean county enrollee in conventional Medicare, plus changes together with quartile funds and high quality bonuses. The chance-adjusted benchmark additionally takes into account an enrolleeŌĆÖs well being.

Samantha Randall at USC, CC BY-ND

Concept as opposed to truth

In concept, this cost machine will have to save the Medicare machine cash for the reason that risk-adjusted benchmark that Medicare estimates for every plan will have to run, on moderate, equivalent to what Medicare would in truth spend on a planŌĆÖs enrollees if theyŌĆÖd enrolled in conventional Medicare as a substitute.

If truth be told, the risk-adjusted benchmark estimates are some distance above conventional Medicare prices. This reasons Medicare ŌĆō in reality, taxpayers ŌĆō to spend extra for every one that is enrolled in Medicare Benefit than if that individual had enrolled in conventional Medicare.

Why are cost estimates so top? There are two major culprits: benchmark changes designed to inspire Medicare Benefit plan availability, and menace changes that overestimate how ill Medicare Benefit enrollees are.

Prime risk-adjusted benchmarks result in overpayments from the govt to the personal firms that administer Medicare Benefit plans.

Samantha Randall at USC, CC BY-ND

Benchmark changes

Because the present Medicare Benefit cost machine began in 2006, policymaker changes have made MedicareŌĆÖs benchmark estimates much less tied to what the plan spends on every enrollee.

In 2012, as a part of the Inexpensive Care Act, Medicare Benefit benchmark estimates won some other layer: ŌĆ£quartile adjustments.ŌĆØ Those made the benchmark estimates, and due to this fact funds to Medicare Benefit firms, greater in spaces with low conventional Medicare spending and decrease in spaces with top conventional Medicare spending. This benchmark adjustment used to be intended to inspire extra equitable get right of entry to to Medicare Benefit choices.

In that very same yr, Medicare Benefit plans began receiving ŌĆ£quality bonus paymentsŌĆØ with plans that experience greater ŌĆ£star ratingsŌĆØ in line with high quality components akin to enrollee well being results and take care of persistent stipulations receiving greater bonuses.

Alternatively, analysis presentations that scores have now not essentially progressed high quality and will have exacerbated racial inequality.

Even prior to absolutely bearing in mind menace adjustment, contemporary estimates peg the benchmarks, on moderate, as 8% greater than moderate conventional Medicare spending. Which means that a Medicare Benefit planŌĆÖs spending estimate might be under the benchmark and the plan would nonetheless receives a commission extra for its enrollees than it might have charge the govt to hide those self same enrollees in conventional Medicare.

Overestimating enrollee illness

The second one main supply of overpayment is well being menace adjustment, which has a tendency to overestimate how ill Medicare Benefit enrollees are.

Each and every yr, Medicare research conventional Medicare diagnoses, akin to diabetes, melancholy and arthritis, to know that have greater remedy prices. Medicare makes use of this knowledge to regulate its funds for Medicare Benefit plans. Bills are diminished for plans with decrease predicted prices in line with diagnoses and raised for plans with greater predicted prices. This procedure is referred to as menace adjustment.

However thereŌĆÖs a vital bias baked into menace adjustment. Medicare Benefit firms know that theyŌĆÖre paid extra if their enrollees appear extra ill, in order that they diligently be sure that every enrollee has as many diagnoses recorded as conceivable.

This will come with felony actions like reviewing enrollee charts to make sure that diagnoses are recorded appropriately. It may well additionally every now and then entail outright fraud, the place charts are ŌĆ£upcodedŌĆØ to incorporate diagnoses that sufferers donŌĆÖt in truth have.

In conventional Medicare, maximum suppliers ŌĆō the exception being Responsible Care Organizations ŌĆō donŌĆÖt seem to be paid extra for recording diagnoses. This distinction signifies that the similar beneficiary is more likely to have fewer recorded diagnoses if theyŌĆÖre enrolled in conventional Medicare quite than a non-public insurerŌĆÖs Medicare Benefit plan. Coverage professionals consult with this phenomenon as a distinction in ŌĆ£coding intensityŌĆØ between Medicare Benefit and conventional Medicare.

The similar individual may be documented with extra diseases in the event that they join in Medicare Benefit quite than conventional Medicare ŌĆō and value taxpayers extra money.

Samantha Randall at USC, CC BY-ND

As well as, Medicare Benefit plans continuously attempt to recruit beneficiaries whose well being care prices will likely be not up to their diagnoses would are expecting, akin to any person with an overly delicate type of arthritis. That is referred to as ŌĆ£favorable selection.ŌĆØ

The diversities in coding and favorable variety make beneficiaries glance sicker after they join in Medicare Benefit as a substitute of conventional Medicare. This makes charge estimates greater than they will have to be. Analysis presentations that this mismatch ŌĆō and ensuing overpayment ŌĆō is most probably most effective going to worsen as Medicare Benefit grows.

The place the cash is going

One of the extra funds to Medicare Benefit are returned to enrollees thru further advantages, funded via rebates. Further advantages come with cost-sharing discounts for hospital therapy and pharmaceuticals, decrease Section B and D premiums, and additional ŌĆ£supplemental benefitsŌĆØ like listening to aids and dental care that conventional Medicare doesnŌĆÖt duvet.

Medicare Benefit enrollees might experience those advantages, which might be thought to be a praise for enrolling in Medicare Benefit, which, in contrast to conventional Medicare, has prior authorization necessities and restricted supplier networks.

Alternatively, in accordance to a couple coverage professionals, the present potential of investment those further advantages is unnecessarily dear and inequitable.

It additionally makes it tricky for normal Medicare to compete with Medicare Benefit.

Conventional Medicare, which has a tendency to price the Medicare program much less in step with enrollee, is most effective allowed to give you the usual Medicare advantages bundle. If its enrollees need dental protection or listening to aids, theyŌĆÖve to buy those one at a time, along a Section D plan for pharmaceuticals and a Medigap plan to decrease their deductibles and co-payments.

Medicare Benefit plans be offering extras, however at a top charge to the Medicare machine ŌĆō and taxpayers. Simplest 50-60 cents of a greenback spent is returned to enrollees as diminished prices or greater advantages.

AP Photograph/Pablo Martinez Monsivais

The machine units up Medicare Benefit plans not to most effective be overpaid but additionally be increasingly more common, all at the taxpayersŌĆÖ dime. Plans closely promote it to potential enrollees who, as soon as enrolled in Medicare Benefit, will most probably have problem switching into conventional Medicare, even supposing they make a decision the additional advantages donŌĆÖt seem to be well worth the prior authorization hassles and the restricted supplier networks. By contrast, conventional Medicare most often does now not have interaction in as a lot direct promoting. The government most effective accounts for 7% of Medicare-related advertisements.

On the similar time, some individuals who want extra well being care and are having hassle getting it thru their Medicare Benefit plan ŌĆō and are in a position to modify again to conventional Medicare ŌĆō are doing so, in step with an investigation via The Wall Side road Magazine. This leaves taxpayers to select up take care of those sufferers simply as their wishes upward thrust.

The place will we pass from right here?

Many researchers have proposed tactics to scale back extra authorities spending on Medicare Benefit, together with increasing menace adjustment audits, lowering or getting rid of high quality bonus funds or the usage of extra information to make stronger benchmark estimates of enrollee prices. Others have proposed much more basic reforms to the Medicare Benefit cost machine, together with converting the foundation of plan funds in order that Medicare Benefit plans will compete extra with every different.

Lowering funds to plans might must be traded off with discounts in plan advantages, although projections recommend the discounts can be modest.

ThereŌĆÖs a long-running debate over what form of protection will have to be required beneath each conventional Medicare and Medicare Benefit. Just lately, coverage professionals have advocated for introducing an out-of-pocket most to conventional Medicare. There have additionally been a couple of unsuccessful efforts to make dental, imaginative and prescient, and listening to products and services a part of the usual Medicare advantages bundle.

Even supposing all older folks require common dental care and lots of of them require listening to aids, offering those advantages to everybody enrolled in conventional Medicare would now not be reasonable. One method to offering those necessary advantages with out considerably elevating prices is to make those advantages means-tested. This might permit folks with decrease earning to buy them at a lower cost than higher-income folks. Alternatively, means-testing in Medicare may also be arguable.

There may be debate over how a lot Medicare Benefit plans will have to be allowed to change. The common Medicare beneficiary has over 40 Medicare Benefit plans to choose between, making it overwhelming to check plans. For example, at the moment, the typical individual eligible for Medicare must sift in the course of the positive print of dozens of various plans to check necessary components, akin to out-of-pocket maximums for hospital therapy, protection for dental cleanings, cost-sharing for inpatient remains, and supplier networks.

Even supposing thousands and thousands of persons are in suboptimal plans, 70% of folks donŌĆÖt even examine plans, let by myself transfer plans, throughout the once a year enrollment length on the finish of the yr, most probably for the reason that technique of evaluating plans and switching is hard, particularly for older American citizens.

MedPAC, a congressional advising committee, means that proscribing variation in sure necessary advantages, like out-of-pocket maximums and dental, imaginative and prescient and listening to advantages, may just lend a hand the plan variety procedure paintings higher, whilst nonetheless taking into account flexibility in different advantages. The problem is determining methods to standardize with out unduly lowering customersŌĆÖ choices.

The Medicare Benefit program enrolls over part of Medicare beneficiaries. Alternatively, the $83-billion-per-year overpayment of plans, which quantities to greater than 8% of MedicareŌĆÖs general price range, is unsustainable. We imagine the Medicare Benefit cost machine wishes a extensive reform that aligns insurersŌĆÖ incentives with the desires of Medicare beneficiaries and American taxpayers.

This text is a part of an occasional sequence analyzing the U.S. Medicare machine.

Previous articles within the sequence:

Medicare vs. Medicare Benefit: gross sales pitches are continuously from biased assets, the selections may also be overwhelming and unbiased lend a hand isnŌĆÖt similarly to be had to all

{kind=link}